Tax Basis Period Reform: How will this affect your business and tax affairs?

· Posted on: May 15th 2024 · read

Many sole traders and partnerships, including Limited Liability Partnerships (LLPs) are going to be affected by tax changes that are going to be taking place by way of a reform to the existing basis period method of taxation. At the time of writing it is expected that the reforms will be fully effective from the 24/25 tax year, with 23/24 being a transition year.

These changes will affect all sole traders, unincorporated partnerships and LLPs who currently do not prepare their annual accounts to a reference date ending between 31 March and 5 April.

Current continuing businesses

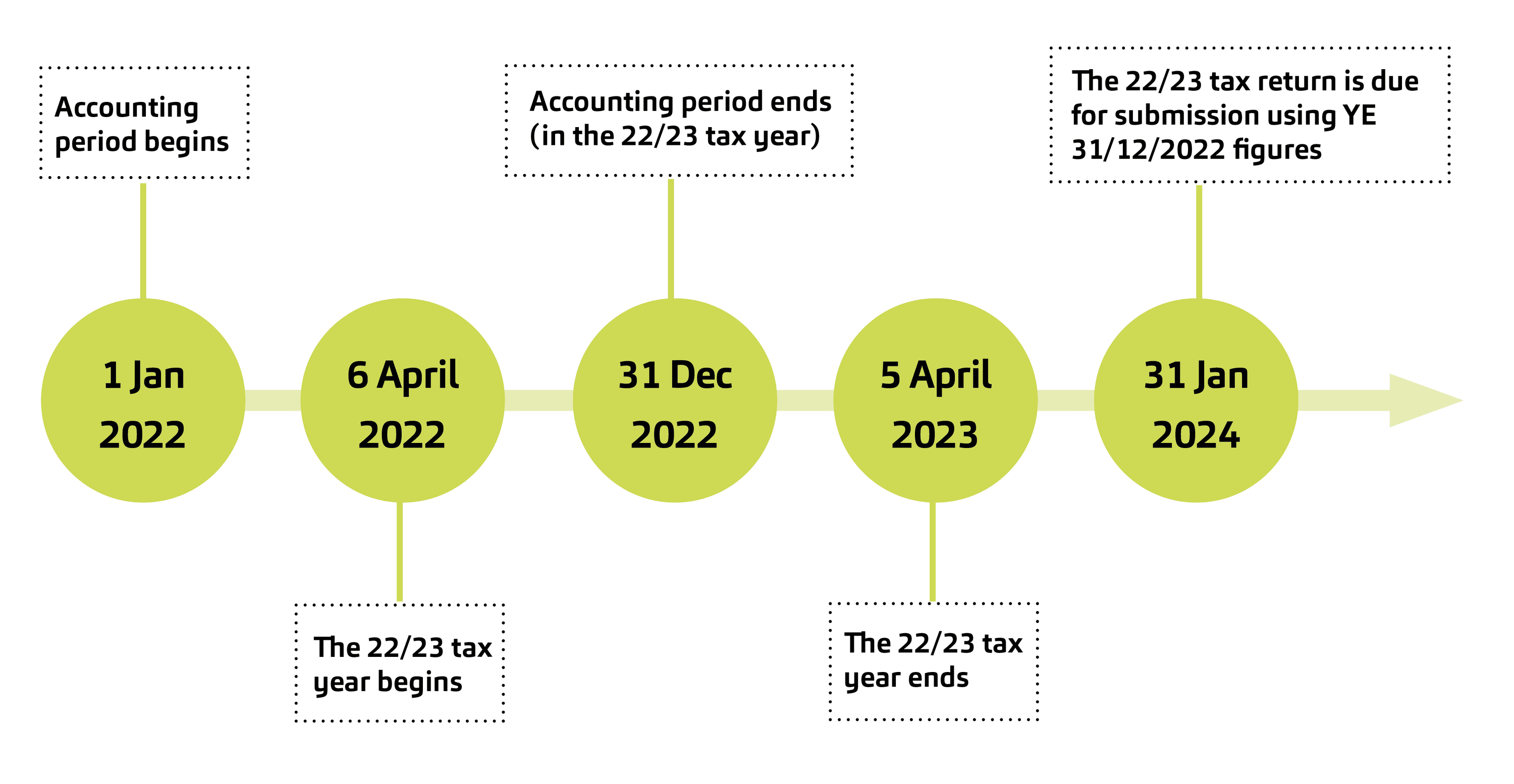

The current basis period rules mean that established sole traders and partners/members in ongoing businesses pay tax based on the financial performance of the business in the 12-month accounting period which ends in the tax year.

For example, if a business prepares accounts for the 12 months ending 31 December 2022, and this is not the first period of account, then the profits from this period, after adjustments, would be taxed on the individual in their tax return for the 2022/23 tax year.

Current opening year rules

Different rules apply to individuals in the first tax year that they commence to trade. Partners or members are typically treated as commencing to trade on the date that they are admitted into the partnership/LLP.

In their first tax year of trade an individual is taxed on their profits from the date of starting to trade to the end of that tax year, being 5 April.

For example, a new partner joins on 1 January 2021, where the accounting year end is 31 December. The first period that they are taxed is 2020/21, with income being their profits from 1 January 2021 to 5 April 2021.

The next tax year, 2021/22 they are taxed on the first 12 months profits, being 1 January 2021 to 31 December 2021. There is a portion of profits taxed twice in these tax years, and this is known as “overlap profit”.

Proposed new basis period method of taxation rules

The new rules dictate that, from 2024/25 all unincorporated businesses will be taxed on the profits generated between the start and end of the tax year, from 6 April to 5 April. This will apply regardless of the year-end that the business prepares its accounts to. But HMRC do allow a year end that falls between 31 March and 5 April to be treated as if it falls at the end of the tax year.

So if a business has an accounting year end of 31 December it will have to apportion profits from two accounting periods to fit into the 6 April to 5 April timeline. If the accounts have not been finalised before the tax return filing deadline, then estimated profits will have to be included.

Tax year 23/24 - the transition year

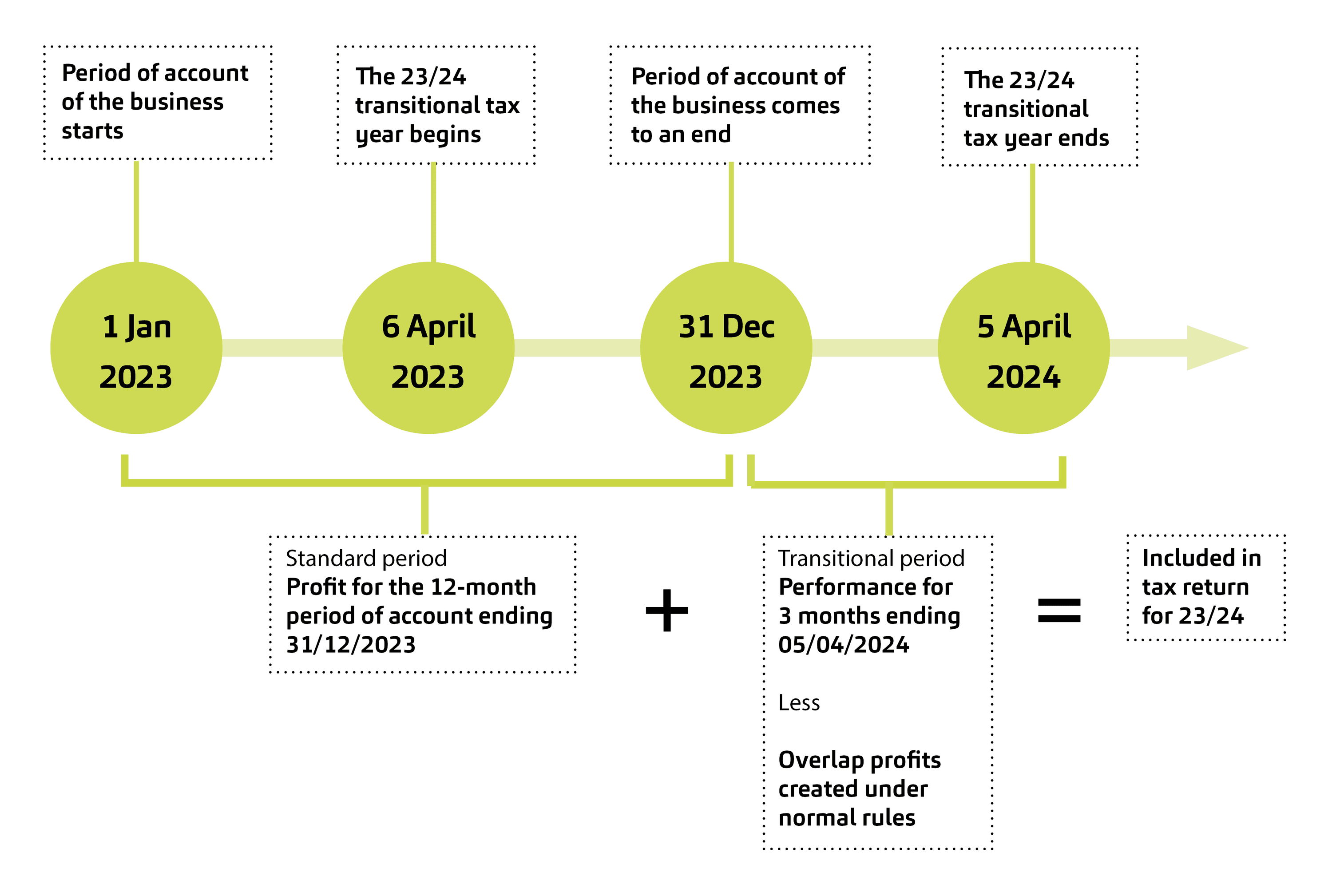

2023/24 will be the key tax year when it comes to these proposed new rules, as this will be the year of transition. In this tax year, the individuals will be taxed on a long period of account ending 5 April 2024, such that this period picks up all untaxed accounting profits generated up to this date, which is termed ‘transition profits’. Relief will be given for any overlap profits generated under the current basis period rules.

In our example of an ongoing 31 December accounting year end, in 2023/24 the tax return will have to include profits for the 12 months ended 31 December 2023 plus profits for 3 months ended 5 April.

Please note that transition profits are ignored when determining a taxpayers income for personal allowance abatement (where income exceeds £100,000) and high income child benefit charge (HICBC) purposes (where income exceeds £50,000).

Estimated figures

As shown in the diagram above, the profits in the 3 months to 5 April 2024 will fall in the 31 December 2024 accounting year but will need to be included in the 2023/24 tax return, the submission of which will still remain at 31 January following the end of the tax year (so 31 January 2025 in this case). As a result, this leaves the prospect of the profits in the 3 months to 5 April 2024 having to be estimated to comply with the submission deadline of the 2023/24 tax return, as the accounts for the year ended 31 December 2024 are unlikely to be finalised ahead of the filing date.

One solution is to change the year end to 31 March/5 April so the tax year and accounting year align. However, this may not be the most commercially viable solution for several reasons.

Without changing the accounting date, businesses must make amendments to prior year tax returns where estimated figures have been used ‘without delay’. If the figures originally used were the best estimate at the time of completing the return, then it is unlikely that penalties will be charged if the final tax due turns out to be higher than originally estimated (although interest will incur on underpayments).

Businesses will be allowed to amend provisional figures within the normal time limits for submitting amended returns, which varies depending on if the original submission deadline had been met. Effectively, this means that businesses are likely to have to always file an amended return along with the usual tax return for that year, unless the amended return is filed sooner. We understand this presents a compliance and cost burden to businesses, but it is the necessary route to take if changing the accounting year is not a feasible option.

Transitional profit spreading

There are rules that determine that the payment of the tax liability generated from transitional period profits to be spread over 5 tax years beginning with the year of transition. This is the default position from HMRC’s perspective, and this should ease cashflow by ensuring the extra tax due on these profits is not paid entirely in 2023/24.

Although spreading is the default position, in the years 2023/24 to 2026/27, it will be possible to advance the assessment of transition profits from later years into the current year via an election on the tax return. This will be worthwhile, for example, if the profits of a year are lower than normal, such that advancing spread profits from a later year will use up the basic rate band or personal allowance that would otherwise be unused.

Overlap profits

Overlap profits may have arisen on commencements of trade or, for very old businesses, when they transitioned to the current year basis of assessment in the 1990s. These profits will be set off when calculating profits for the transition year (2023/24). Where a taxpayer or agent does not have a record of overlap profits, HMRC can provide details on request if these figures are recorded on their systems.

On 29 August 2023, HMRC launched an online tool that will allow businesses and their agents to request details of overlap profits, where that data is held by HMRC. An online form is available, with submissions processed by a dedicated team at HMRC, who will then respond by email.

Conclusion

Individuals should be reviewing their future tax liabilities, and when and how they will become payable to ensure any potential cash flow issues are managed. We also have the opportunity to plan with businesses any change to their accounting year ends that may reduce the administrative burden that these new rules may create.

Get in touch

To discuss this topic further and how these changes may impact you and your business, or for any questions on personal tax matters, please contact our tax team.